2023 Was an Outlier... Here’s Why

- Backtesting is one of the best ways to prove the validity of an investment strategy — but without the proper parameters, a backtest can be misleading. When choosing a fund manager, investors should look for a clearly codified systematic strategy.

- Trend following looks at medium and long-term market movements on a global macro scale. Global uncertainty creates trading opportunities.

- Structural inflation and geopolitical conflicts are among the factors suggesting that 2023’s stock market performance was an outlier year in a larger macro trend.

Hindsight is 20/20 — or, in the case of systematic investing, hindsight provides the data-driven insights that inform a strategic portfolio allocation. But backtesting, the process of using historical data to evaluate an investment strategy, is more complicated than regretting not buying up shares of Apple and Amazon back in 1997.

“If somebody came to you and said, these are the stocks I would’ve bought ten years ago, laugh them out of the room,” advises Andrew Beer. Nobody’s clairvoyant, and a sustainable investment strategy needs more than just a lucky hunch. It’s why every investment podcast comes tagged with the disclaimer that past performance is not indicative of future results.

This reminder is especially relevant as we come off a year of a 24% return on the S&P 500, a bond yield rally and a renewed confidence that central bank tightening has avoided a global recession. Are we out of the woods, or was 2023 perhaps an anomaly in a larger global macro trend that’s been brewing since the COVID-19 pandemic?

To answer this question, our Top Traders Unplugged co-hosts came together on a special edition of the Systematic Investor Series to discuss how trend-following strategies should react to a year of positive returns amidst continued inflation, geopolitical conflicts and market volatility. For both active traders and investors seeking a fund manager, here’s a framework for understanding how current global trends may impact investment strategy in the coming years.

The trend-following profile

Trend following, in overly simplistic terms, buys when price action is moving up and sells when price action is moving down. In addition to price, Alan Dunne adds two other characteristics of a trend-following strategy.

“We’re talking about a medium- to long-term timeframe, and we’re talking about trading in the direction of the prevailing medium- to long-term trend,” he says.

Medium- to long-term, in this case, typically refers to a few weeks or a few months, as opposed to a short-term strategy with a five to 10-day average hold period.

Other market data, such as a yield curve or economic time series, is more commonly associated with a macro strategy where risk is managed differently and managers are looking to capture a few big moves rather than many small gains across a highly diversified portfolio. The semantics matter because a true trend-following strategy will account for unexpected market movements better than a more rigid portfolio allocation.

“[Trend following] should be more predictable in that it should reflect some underlying economic rationale as to why you’re able to extract excess returns at very specific moments in time but not get killed the rest of the time,” Andrew explains.

Non-trend, on the other hand, might involve a sound global macro strategy that ends up having a terrible year. Case in point, many investors were convinced interest rates would drop in 2022, and when they didn’t, the U.S. bond market tanked.

“Trend as a strategy is long macro uncertainty and is always going to be highly correlated to macro themes no matter what they are,” adds Katy Kaminski. “[Trend following] is macro exposure in a liquid and less manager-specific and thesis-specific way.” This especially matters because investment theses can be overly reliant on historical data: the backtest.

Ingredients of a backtest

Financial managers are prone to survivorship bias — focusing too much on winning trades and ignoring the ones that “didn’t survive.” This can sometimes come across in the presentation of a misleading or incomplete backtest. The biased conclusions may even be unintentional, just the results of poorly informed methodologies. Imagine making an annual retail sales forecast only based on numbers from Black Friday or packing for a trip in January based on the average weather in July.

Mark Rzepczynski says, “You get the comment from a lot of investors, ‘Well, I’ve never met a bad backtest in my life.’” This is the tongue-in-cheek observation that market simulation differs from trading reality, and that many backtesting methods fail to account for all of the real-world variables that can impact portfolio performance. Although no backtesting method is perfect, strong models do share a few key ingredients.

Systematic strategy

Firstly, a backtest should represent a systematic, disciplined approach. The strategy should have clearly defined parameters and trading signals, but it’s important to not cherry-pick conditions that wouldn’t have fit the likely real-time decision of the historical period. For example, it would be easy to say a good strategy is to short the market when there’s news of a pandemic — look how well that would have done in February 2020! But realistically, that can’t be a consistently applied approach.

Andrew advises that backtesting should account for some poor decision-making. “Pick the dumbest factor sets and see if they work,” he says. If a backtest proves so sensitive that a single parameter change at the margin drastically throws off the results, it’s not a good investment strategy.

Furthermore, Rob Carver says to look for a correlated pattern of returns, such as a trend-following fund performing well during periods when other trend-following funds were also successful. “I’d also be looking at other distributional properties apart from just the straight-out Sharpe ratio,” he adds, referring to the common measurement of risk-adjusted return. Trading futures, for instance, involves more leverage, so if the actual risk is high even on a great return, it may not fit an investor’s risk appetite.

Parameter correlation

Secondly, when studying a backtest, it’s vital to understand how parameters are correlated. Katy notes, “It’s really easy to replicate correlation but not easy to replicate returns.” In other words, a technical analysis doesn’t always equate to real-world profits.

Consider a simple moving average (SMA) model that shows a particular industry trending upward over a period of several months. While this can be informative to an extent, the SMA inherently lags behind recent data and trends, resulting in a sort of overfitting to the historical numbers that fail to predict where the industry is moving next. If an investment strategy is strongly correlated to this moving average in the backtested data, it may not deliver the same results in practice.

Instead, the ideal system should change as markets shift over time. “Really the goal is parameter diversification,” Katie says. Investors shouldn’t create an overreliance on a particular correlation, particularly if it’s not delivering a strong risk-adjusted return with recent market data.

Long-term view

Finally, a sound strategy takes a long-term view. Cem Karsan says, “Markets are very much a voting machine in the short term. It has much more to do with flows and supply and demand [than macro trends].”

Backtesting, then, can be fallacious when the historical data doesn’t stretch back far enough. Energy products are an easy example. In the short term, prices can be highly volatile based on present supply and demand, but the years-long view considers the global outlook of oil and gas usage versus alternatively sourced renewable energy.

“Market structure changes and is constantly evolving,” Cem adds. A systematic investment strategy needs to maintain the flexibility to respond to different scenarios and conditions.

Was 2023 an outlier?

So, when we look back systematically with a wide-angle lens, can we say that the market conditions of 2023 are likely indicative of the next few years? In short, our experts say no.

Inflation comes to mind. Alan says, “People are suddenly forgetting about all of those structural headwinds that policymakers pointed to [in 2022] in relation to supply chains and nearshoring and deglobalization, the things that we think might push up inflation and make it stickier over time.”

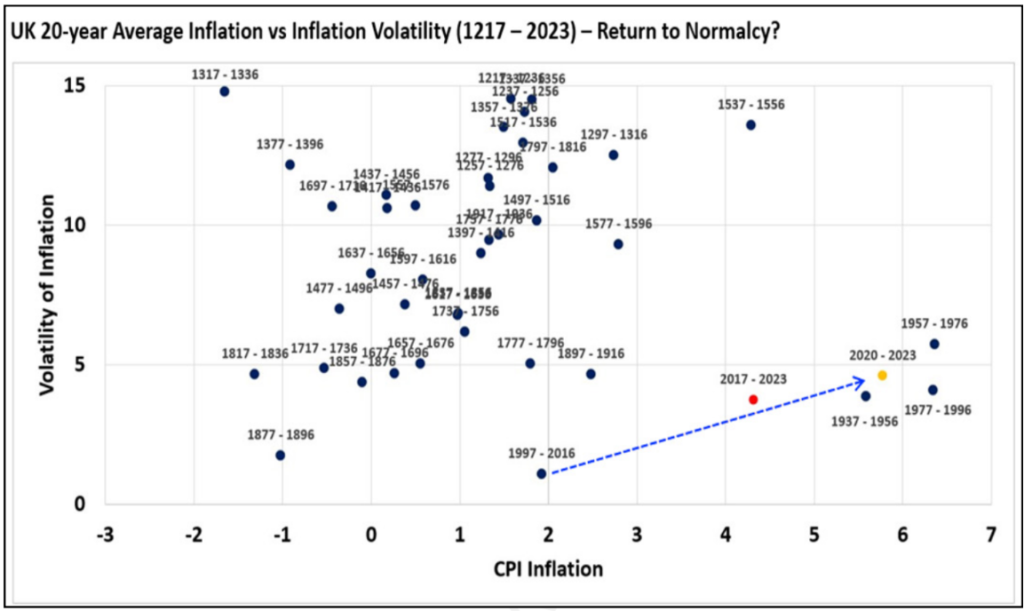

While our recent memory suggests that low inflation is the norm, research from the Bank of England demonstrates how most of the 21st century has been atypical in that regard. “Basically [the data] shows what an outlier the last 20 years have been in terms of inflation being on target and not fluctuating … historically we’ve seen much more variation in inflation,” Alan explains.

Cem points to deglobalization as a new force adding inflationary pressure as well as a cultural war against the financial inequality that was exacerbated by a loose monetary policy disproportionately benefiting wealthy investors. Younger generations in particular may drive forward political ideologies focused on corporate regulation or social safety nets.

Adding to the mix, Andrew describes the present geopolitical situation. “We have a land war in Eastern Europe, we have the potential for war in the Middle East. We have taken a certain level of [global] stability for granted since World War II,” he says. Moving forward, he expects more volatility to follow these conflicts.

All that’s to say, after a year of apparent market correction many of the themes of populism and seismic restructuring of supply chains are still at play. Cem notes that taking 2022 and 2023’s market performance together looks reminiscent of market performance from 1968-1982. “We had structural inflation yet cyclical downturns,” he says. This period of global economic stagnation certainly casts a long shadow over the remainder of the 2020s.

Ditching 60/40

Considering these market influences, how should investors respond? To start, the classic 60/40 portfolio allocation may be an outdated strategy. In the 2010s, Andrew says, “[The 60/40 portfolio] outperformed 98.5% of hedge funds over the course of a decade. But the underlying assumption was that stock and bond correlations would remain negative.”

A high-inflation, high-volatility environment is likely to drive a positive correlation between stocks and bonds. Inflation lowers the value of future returns on fixed income, lowering bond prices, and economic uncertainty simultaneously drags down the equities market.

This is the opportunity for trend followers who are essentially regime-agnostic. It doesn’t matter if we’re in a bull market, bear market or something in between because a trend-following strategy trades on volatility. A dynamically adjusted portfolio is a natural response to entropy and accelerating chaos.

“I think the most important thing when looking to the future is not to try to predict an outcome but to try to predict the distribution of potential outcomes,” says Cem. As investors look ahead in 2024 and beyond, the focus should be less on fitting models around historical data and more on taking a diversified approach to prepare for the unpredictable.

This is based on an episode of Top Traders Unplugged, a bi-weekly podcast with the most interesting and experienced investors, economists, traders and thought leaders in the world. Sign up to our Newsletter or Subscribe on your preferred podcast platform so that you don’t miss out on future episodes.

Most Comprehensive Guide to the Best Investment Books of All Time

Most Comprehensive Guide to the Best Investment Books of All Time

Get the most comprehensive guide to over 600 of the BEST investment books, with insights, and learn from some of the wisest and most accomplished investors in the world. A collection of MUST READ books carefully selected for you. Get it now absolutely FREE!

Get Your FREE Guide HERE!