- The inverted yield curve on U.S. Treasury bonds could signal a recession. Investors are looking to protect capital and replace fixed income.

- The macroeconomic conditions of the past several years make the case for alternative investments, particularly in real estate and private equity.

- Diversification is the safest play in a volatile market. Chief market strategist Troy Gayeski says exposure to multi-strategy hedge funds may be a good starting point for investors wanting to broaden their liquid portfolios.

After the electric bull market of 2020-21, bolstered by government stimulus and post-pandemic spending, murmurs of recession are growing. We’ve seen 11 rate hikes from the Fed in the last 18 months, and after the historically awful 2022 for U.S. bonds, the asset class is still struggling while the equities market is volatile.

Meanwhile, alternative or “alt” investments are more accessible than ever. The democratization of retail investing means alternatives are no longer an exclusive feature of multi-billion-dollar institutions. Even novice investors can explore a multi-strategy approach beyond the traditional 60/40 split of stocks and bonds.

To shed some light on alt investments, host Alan Dunne spoke to Troy Gayeski, Chief Market Strategist for FS Investments. FS is a global alternative asset manager holding more than $75 billion for a wide range of institutional and individual clients.

“Originally the firm was focused on middle market corporate lending,” Troy says. “It evolved into broader asset classes, senior commercial real estate lending, multi-strategy and tax loss allocation.”

It’s an impressive suite of products consistently delivering upper-quartile performance in their respective strategies. But Troy reminds us that you don’t need a billion-dollar portfolio to wade into alternatives.

Real estate investment trusts (REITs) and master limited partnerships (MLPs) are just two examples of wealth management alternatives available to individual investors. Troy advises clients to step out of the 60/40 framework and include an alt allocation in their portfolios.

Whether it’s 5% or 20%, Troy says, “[the alternative allocation] should certainly be higher than it was five years ago.”

What’s the advantage of alts, and why are they trending in the last few years? Troy revealed his thought process on the Top Traders Unplugged Allocator Series. Here’s what every investor should know.

Stocks: high risk, limited reward

It’s the question we’ve been asking for a year and a half. Is a recession coming?

Troy calls 2020-21 “one of the greatest greenlight-go, risk-taking environments in history.” Stimulus money rained down on America and the stock market could do no wrong — until the correction came, and 2022 was the worst year for U.S. stocks since the global financial crisis of 2008.

Yet despite the Fed’s aggressive rate hikes, the failure of four U.S. banks and continued inflation, the economy has been resilient. This is a conundrum for investors.

On one hand, it seems the so-called “soft landing” of the Fed’s rate policies is achievable. Troy names increased government spending under the Inflation Reduction Act and positive trends in the housing market’s contribution to GDP as two indicators that the U.S. could avoid a recession. In this case, portfolios that are overweight in equities could see some near-term upside.

Then again, recession fears will also be a headwind for stocks. Troy says, “As you look forward, recession risk is dramatically higher today than really any time since pre-[2008]. So that obviously will work to the detriment of equity markets.”

While many stocks are trading below fair-market valuation, risk-free cash investments are seeing the highest returns they’ve had in 20 years and could even go higher. Considering the incentive to cash out, the equities market looks overvalued according to Troy.

“From a relative basis, we’ve only been more overvalued in the dot-com bubble,” he adds.

The upside-down bond market

Here’s the other side of the 60/40. Bonds historically outperform stocks during a recession, so they would intuitively seem like a safe strategy. The problem? Yields are inverted.

“We’ve still got a massively inverted yield curve,” Troy explains, “which really destroys the incentive to create credit for any longer-maturity loans.”

An inverted curve happens when interest rates are higher on shorter-term bonds compared to their counterparts with longer durations to maturity. As of September, three-month U.S. Treasury bills were paying 1.1% higher than 10-year bonds.

This unusual situation means fixed-income investors actually get better returns on short-duration debt securities than long-term holds. As we stand currently, a certificate of deposit (CD) or even a high-yield savings account earns a better rate than a Treasury note, leading many risk-averse investors to look outside the bond market.

So where does that leave us? Is 60/40 dead? Alan asks, “Given the overall landscape, is there structurally a case for more alternatives?”

Troy says yes, but not all investors should choose the same entry point.

Making the case for alternatives

“It depends on the starting point for the client,” Troy explains, “and how far they are along in embracing alternatives.”

Many institutional investors have moved from the 60/40 benchmark to a 40-30-30 model: 40% equities, 30% bonds, 30% alternatives. Troy says older clients who may prefer a more conservative fixed-income strategy, or credit investors who lack the capital for private debt strategies, likely won’t match the full 30% allocation. But even dipping one’s toes in at a 5-10% portfolio allocation for high-dividend REITs can reap the benefits of an alternative strategy.

Why now? Troy wrote extensively about the galactic mean reversion — the term he coined for the macro-readjustment of overvalued asset classes. Looking back on the past several decades, Troy sees trends of rampant asset inflation, moderate GDP growth and labor market stagnation.

The U.S. saw its real GDP more than double from 1990 to 2022, but that’s nothing compared to the approximately 9% annualized rate of return in the stock market over the same period. The Fed grew the money supply faster than nominal GDP after the 2008 global financial crisis, creating the liquidity to inflate asset prices. If that pattern corrects, we’re likely to see lower highs and lower lows in the equity market.

According to Troy, the imbalance will remain a headwind for return expectations on equities “until we have either a hard landing or some type of market accident.” Even if unemployment increases, it’s unlikely the Fed will scale back recent rate hikes as long as there’s some indication they’re threading the needle to avoid an economic crash. In other words, stocks could be stuck and bonds could remain relatively unattractive.

“Forward return expectations for 60/40 are dramatically lower now than over most of our investment careers,” Troy says. He doesn’t go so far as to predict a lost decade akin to 1999-2009, but investors will need more realistic expectations after the post-pandemic roller coaster. Alts may be the most consistent pathway to growth.

Understanding alternative strategies

With the Fed funds rate rocketing from zero to 5.25-5.5% in the span of eighteen months, Alan asks if investors have become more tactical and defensive.

“The bottom line is that investors should have more cash exposure now than they had when we were in the zero interest rate or reserve policies for years,” Troy explains. But holding cash too long can lead to missed opportunities.

“There’s a lot of inertia in asset allocation,” Troy adds. When investors are moving slowly and looking backward at past performance, it’s tempting to do nothing. Instead, Troy encourages investors to look forward and test which strategies make sense in a mean reversion period.

According to Troy, here are three alternative strategies to consider.

Commercial real estate

As long as the Fed keeps rates elevated, there’s opportunity in floating-rate lending strategies. Specifically, private real estate lending and middle market corporate lending offer a high front-end and protection against the next Fed cut cycle, should we fall into a recession.

“We’re in an environment where LTVs (loan-to-value ratios) are materially lower and spreads are wider [compared to 2021],” Troy says. “You’re getting tremendous love from the front end of the curve, which can persist, at least for another year, if not longer.”

Although metro office towers are in an equity freefall during the age of work-from-home, Troy sees opportunities in lodging, multifamily housing and industrial — namely distribution centers. The high borrowing costs and high cap rates combined with a price decline makes a great entry point for commercial REITs and other real estate credit investments.

Private equity secondaries

Private equity (PE) is generally held by large institutional investors with high fees and a steep barrier to entry historically pricing out individuals. These institutions have policies governing their portfolio allocations and allowable risk thresholds, and, ironically, PE’s outperformance of the stock market has caused many to downsize their positions. Asset owners — such as pensions, sovereign wealth funds or endowments — found their PE allocations overweight and were forced into a portfolio rebalance.

Troy explains, “If you allocated 10% PE, it might be 12 or 13% now. If your investment policy statement says 10, we’ll obviously have to sell down secondary volume to get there.”

The institutional selloff creates an over-supply resulting in a material discount in PE secondaries. Limited partner (LP)-led secondaries are trading at up to a 30% discount to the net asset value (NAV). Although there are still higher costs to entry, a more complex valuation process and less liquidity than other forms of investment, individual accredited investors may find an advantageous buying opportunity in secondary markets.

Liquid strategies

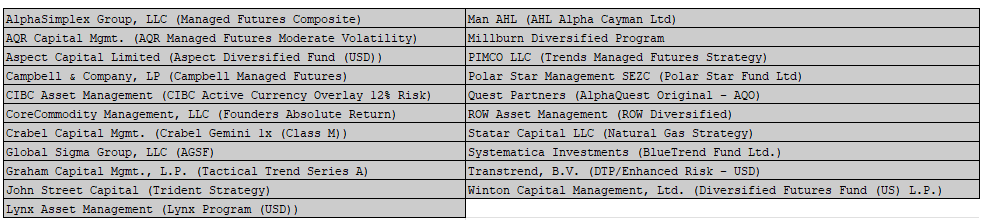

For those wanting more liquidity, Alan asks about other strategies such as a managed futures account or a global macro hedge fund.

“If you’re starting in the liquid space,” Troy advises, “you still want to focus to some extent on hedge funds.” But he offers a word of caution.

“One of the issues with platform hedge funds is that it’s all about supply and demand, and there’s so much demand for that very unique exposure that there’s just not that much supply. The terms have become very investor unfriendly, not just in terms of fees, but in terms of the liquidity profile.”

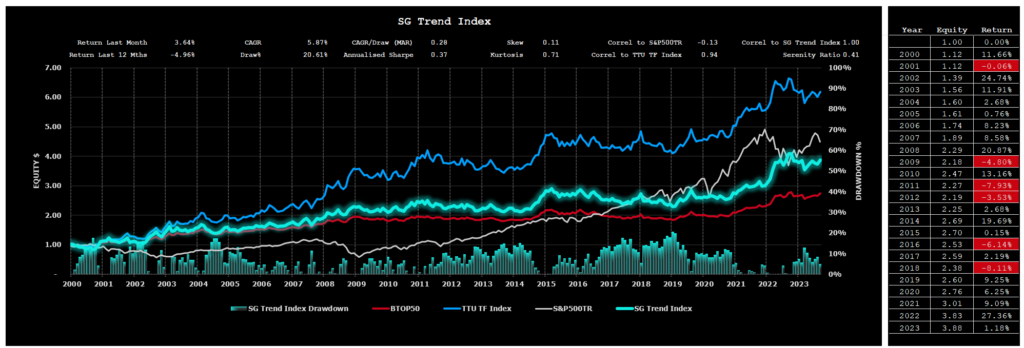

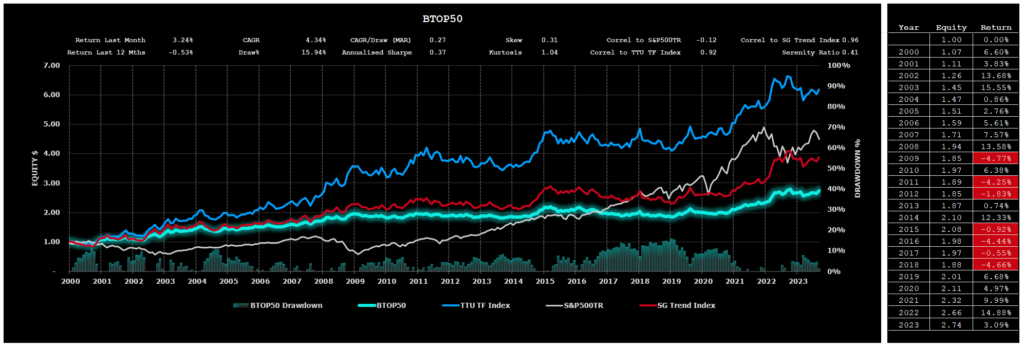

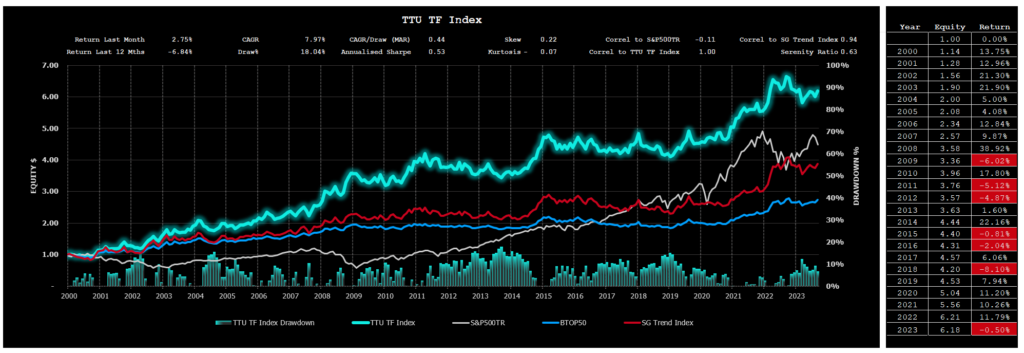

While managed futures funds are typically looking at wild swings based on market volatility, Troy instead recommends a more user-friendly, multi-strategy exposure with lower volatility and low beta. A more consistent returns strategy doesn’t have to time the entry and exit perfectly.

Advice for building a portfolio

All things considered, Troy’s best advice is to be a student of market history. As new geopolitical crises emerge and new innovations disrupt industries and reshape society, market strategies will shift and adjust, but the core principles remain the same.

Troy recommends the late Charles P. Kindleberger’s 1978 classic, “Manias, Panics and Crashes: A History of Financial Crises.” Nearly 50 years later, his economic insights still ring true for market speculation and managing uncertainty. There may be different drivers of corrections and bull markets, but ultimately the cyclical price movements are similar. If you want to learn more about Charles P Kindleberger – read this post.

“Every cycle is different, but every cycle is the same,” Troy says.

No matter what happens in the world, a confident and well-informed strategy can expect long-term gains.

This is based on an episode of Top Traders Unplugged, a bi-weekly podcast with the most interesting and experienced investors, economists, traders and thought leaders in the world. Sign up to our Newsletter or Subscribe on your preferred podcast platform so that you don’t miss out on future episodes.