SVB Carry Crash Increases Deflation Risk…But Not For Long

Investors may get one more chance to buy inflation protection

In The Rise of Carry, which I co-authored with Tim and Jamie Lee, we explained how the growth in carry trades has reshaped the financial markets and global economy. The book was published in late 2019 and contained several assertions that few people grasped at the time, but that are now becoming more mainstream:

1. The Fed’s is losing control:

“…the carry regime creates the sense that central banks are all powerful even as, in a fundamental sense, they are becoming weak.”

2. Big changes to the financial system are on the horizon:

“…the carry regime’s end will also be associated with the end of our current monetary system…”

3. The ability to be long carry – to provide liquidity, to provide leverage – is synonymous with the ability to apply power.

“Carry is a flow from the weak to the strong…Entities that have excess liquidity with which to take risk will lend it, receive carry, and so gain more excess liquidity. Entities that lack liquidity, need liquidity, and must borrow for it, will pay carry and so become more lacking and more needy”.

I plan/hope to write brief notes about all three predictions, but you’ll be relieved to know that today’s only covers the first.

The Carry Regime 101

The basic logic of the carry regime is this – carry trades are leveraged, liquidity providing and short volatility. This means that as they grow, so do financial liabilities of all types. Markets become more liquid temporarily, but also more susceptible to sudden disruption when volatility spikes. When volatility rises, the process reverses itself – markets suddenly become illiquid as private carry traders face losses and retrench. Central banks intervene to provide liquidity and calm markets.

This stems the immediate crises but, below the surface, also serves to truncate losses for carry traders. By truncating losses, central banks encourage further growth in carry trades, requiring larger central bank intervention during the next crisis.

Many commentators have been surprised that Fed intervention and market disruption last week was already bigger than during the Covid crash, but our logic suggests it was exactly what should have been expected.

Central banks are not in control

When we said in 2019 that central banks “are becoming weak” what we mean is that they are not in control of this process. We predicted that the ultimate result of this would be higher, potentially much higher, inflation. Why? Because the immediate danger of a deflationary crisis is always more salient than the longer-term danger of higher inflation. Thus the carry regime grinds forward in rachet-like fashion, pulling central banks along with it.

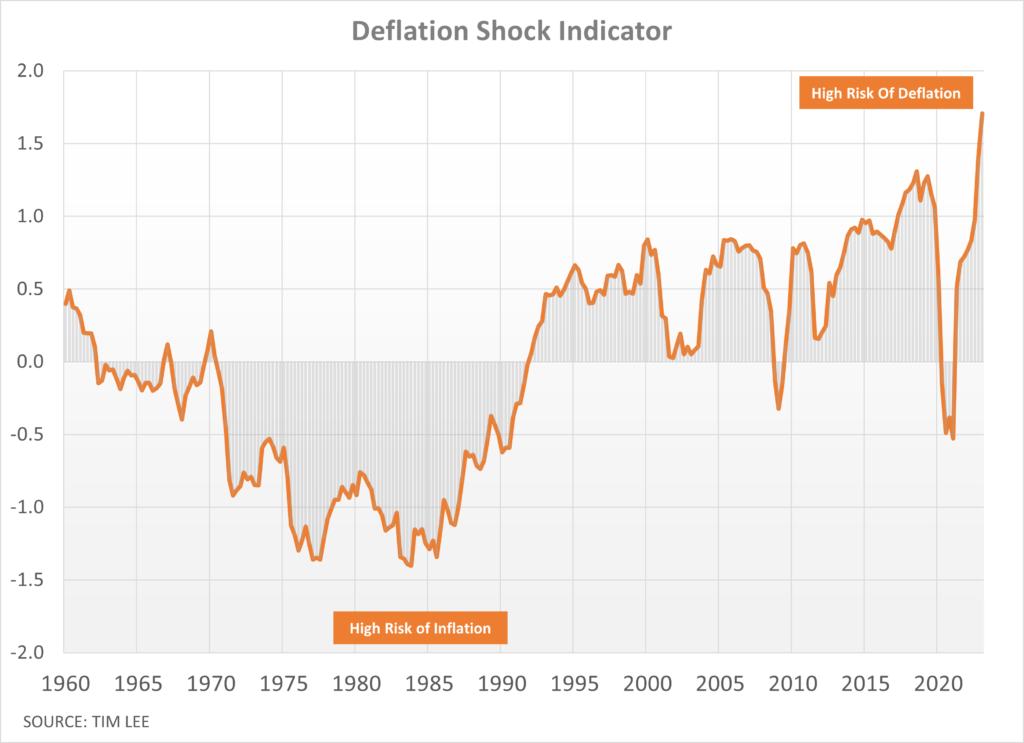

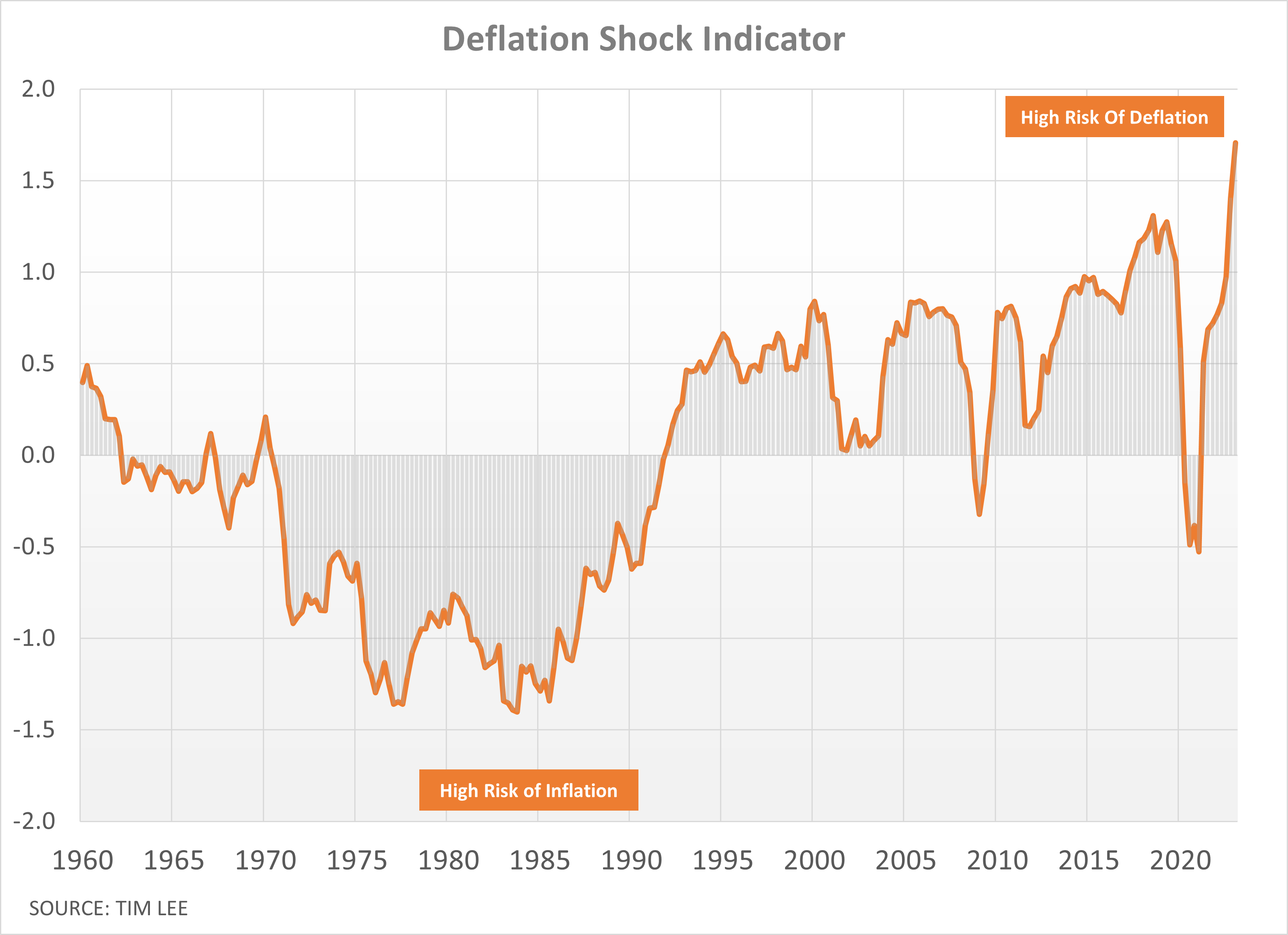

But with each successive crisis the oscillation between deflation and inflation shortens. And that’s why the SVB collapse has increased the prospect for both deflation and inflation. The immediate risk is deflation. Tim Lee has a measure of the potential for a deflationary shock that he has tracked for years. As you can see from the chart below it’s now showing it’s highest ever reading.

{kind=link}

I asked Tim about this over the weekend:

“The main reason for the surge upwards in the indicator, to unprecedented levels, is the collapse of money supply, with my estimate being that for Q1 M2 will be -2.6% year-on-year, unprecedented in modern history.

Some might argue that the indicator is mis-specified because we have been coming off a huge jump in money supply and therefore there could still be an excess of money, in some sense.

But the intuition behind the indicator is that what matters is the present rate of money growth…I think it would be hard to get an inflationary result out of the present conjunction of any possible relevant variables.”

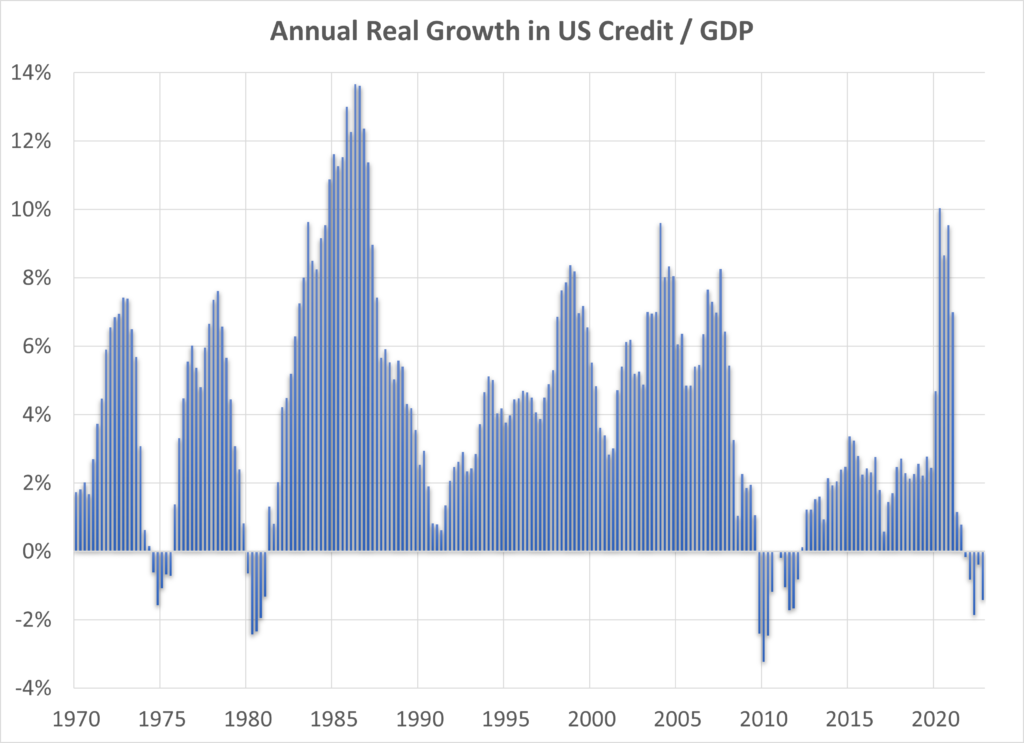

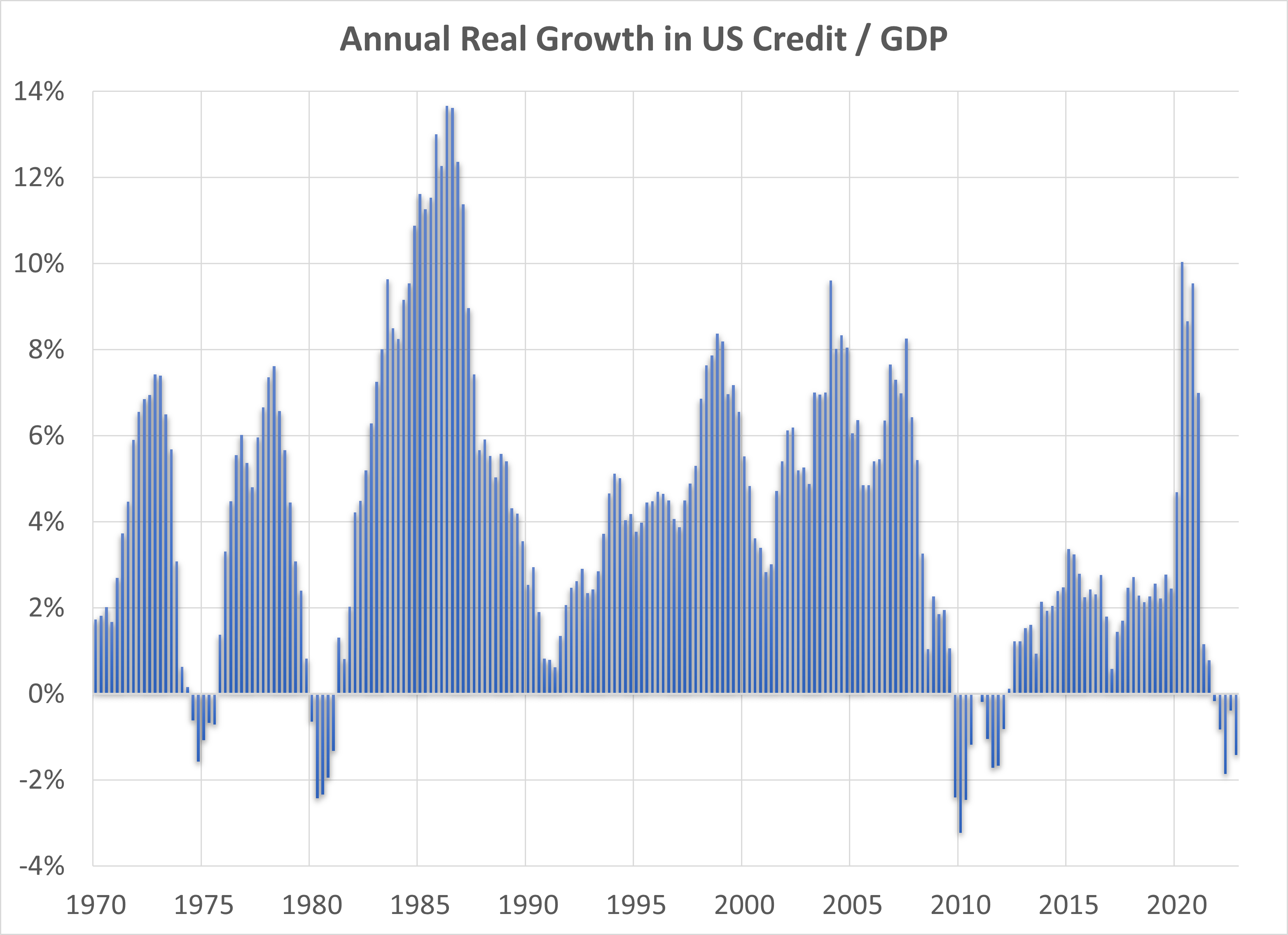

Tim’s measure is also consistent with a proxy for deflation risks that I wrote about after interviewing economist Richard Duncan. Richard believes credit growth is what keeps the economy moving forward and when it falls, as it has over the last year, the Fed either has to respond aggressively or we end up with an recession.

{kind=link}

The last time real credit growth was negative the Fed responded with QE. That eventually dragged the economy forward, but it happened against a backdrop of both cyclical and structural deflationary pressures. Those structural pressures – a “demographic dividend” in the West coupled with lowering of wages from China - are now done. This means the liquidity injections we’ve gotten from the Fed already, and which we are going to continue to get, will increase the risk of inflation.

Give me higher real rates and lower inflation…but not yet

Get ready to hear more debates about whether a particular central bank action is a temporary “market function asset purchase” or a new form of QE. The first major example was last year when British pension funds lost huge amounts on derivative positions caused by rising interest rates.

The Bank of England was intentionally tightening policy to fight inflation. By raising rates the BoE triggered losses in carry trades the pensions had put on. To cover their losses, the funds tried to raise cash by selling bonds. Their selling drove rates even higher, causing more losses and potentially triggering a death spiral. The BoE was forced to say it would buy unlimited quantities of government bonds from them. The offer to buy unlimited quantities of government bonds sounds like quantitative easing.

If you think easing and tightening at the same time sounds like a contradiction, sounds like a loss of control, I’m with you. In the end the BoE “got away with it”. Its argument was that the pension funds were solvent but illiquid and the action was a temporary necessity to bridge the gap before getting back to inflation fighting. But they also deserve credit for posting a transparent post-mortem that acknowledges all of our three points above.

Of course, “solvent but illiquid” is exactly the situation SVB was said to be in. Expect to hear this messaging a lot more in the coming years. The line between market support and QE will become increasingly blurry and, as it does, the risk of much higher inflation will increase.

The underlying fundamentals are this: the carry regime has led to a huge rise in leverage. Raising interest rates and/or tightening financial conditions to fight inflation risks triggering a financial crisis – the deflation shock Tim expects.

Fighting the crisis means increasing the chances of higher inflation. Since crisis risk in more salient and more immediate, it will always get priority. The logical conclusion is that inflation will not return to 2% for a sustained period.

We predicted this in Rise of Carry and the view is no longer controversial, with Larry Fink saying this week that its more likely to be 3.5 - 4.0%. In the short-term, inflation may very well fall, but only temporarily. If it does, use it as an opportunity to buy inflation protection more cheaply. You’ll be glad you did.

This post was written by Kevin Coldiron, Author, Finance Lecturer, Retired Money Manager and co-host on TopTradersUnplugged. Read more of Kevin’s writing on Substack.

Most Comprehensive Guide to the Best Investment Books of All Time

Most Comprehensive Guide to the Best Investment Books of All Time

Get the most comprehensive guide to over 600 of the BEST investment books, with insights, and learn from some of the wisest and most accomplished investors in the world. A collection of MUST READ books carefully selected for you. Get it now absolutely FREE!

Get Your FREE Guide HERE!