Trend Following - Week in Review— May 29, 2026

"Petroleum Complex Extends Lower as Natural Gas Decouples Higher, Equities Set Fresh Records, and the Barometer Drops to Moderately Weak at 32%"

This Week in Trend – 29 May 2026

Welcome to This Week in Trend, your weekly view into the evolving structure of global futures markets and the behaviour of systematic trend following. This edition covers conditions through the close of US markets on Friday, 29 May 2026.

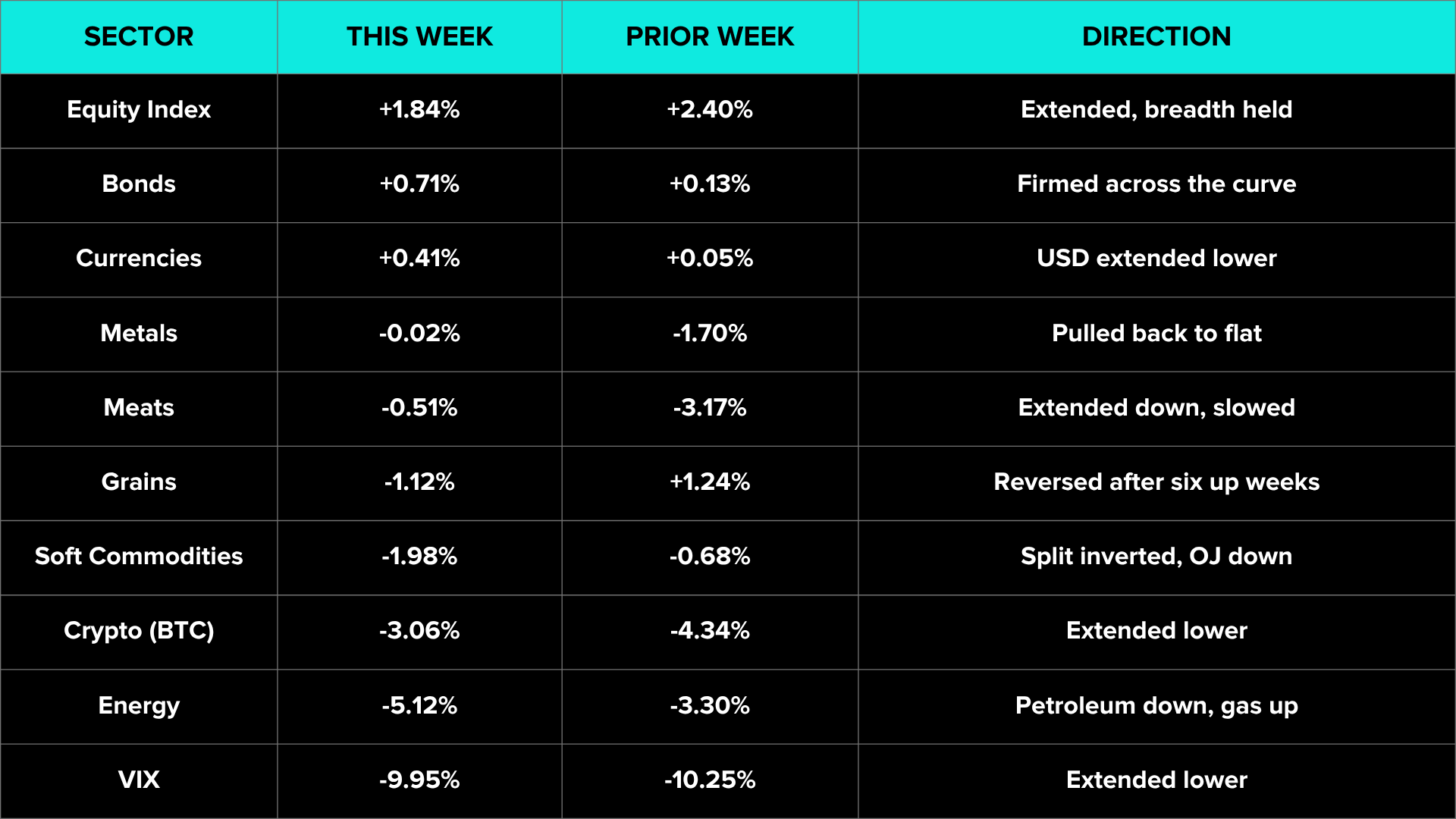

The week extended the prior week’s direction rather than inverting it. The petroleum complex fell for a second consecutive week as market pricing reflected a further unwind of the Middle East war-supply premium: reports indicated returning Middle East production and Strait of Hormuz traffic normalising, even as intermittent strike headlines kept intraday volatility high. Brent settled near 92, down 11.13%, WTI near 88, down 9.57%, Gasoline RBOB down 10.23%, and Heating Oil down 8.06%. Natural Gas broke the other way, up 8.90% and the single largest gain of the week, on reports of a bullish shift in summer cooling-demand forecasts, leaving Energy split at the contract level and down 5.12% on the sector average. The risk tape stayed firm: equity indices averaged +1.84% with all seven contracts higher, the S&P 500 logged its ninth consecutive weekly gain to a fresh record near 7591, the Nasdaq 100 pushed to a new high near 30390, and the VIX fell a further 9.95% to near 17.60.

Inside the complex, the cross-asset picture stayed coherent with a softer-data, softer-dollar tilt. Bonds firmed across the curve at +0.71%, the long end leading (30 Year +1.35%, 10 Year +0.76%) as April PCE printed slightly below expectations on the month and the second-estimate Q1 GDP was revised lighter, easing 10 year yields. The dollar extended lower at -0.34%, with the commodity-linked currencies firmest despite the oil decline (NZD +2.13%, AUD +0.63%). Metals pulled back to roughly flat at -0.02%, Gold firming +0.81% and Copper +0.16% while Silver and Platinum eased. Grains reversed down at -1.12% after six positive weeks, with a wide internal split: Soybean Oil +5.06% and Canola +1.43% against Wheat -5.53% and Corn -3.56%. Soft commodities fell -1.98% on a similar split, Cocoa +3.35% against Orange Juice -7.12%. Meats extended lower at -0.51%, all three contracts down for a second week but on much reduced magnitude. Bitcoin fell 3.06% to near 73,860, extending its drift lower from the January highs.

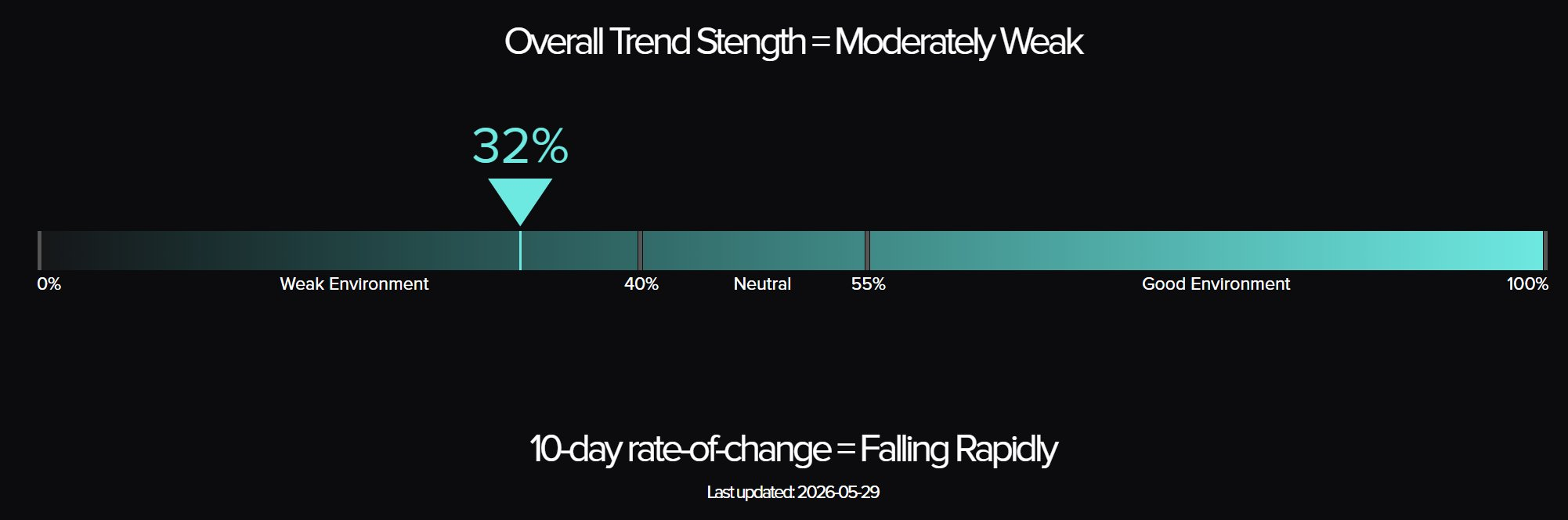

Trend Indicators: Barometer Drops to Moderately Weak, SG Trend Index Erodes

TTU Trend Barometer: 32%, down from 45% last week, with the overall trend strength classification dropping from Neutral to Moderately Weak. The 10-day rate of change has accelerated from “Falling Moderately” to “Falling Rapidly”. The five-week sequence now reads 55, 43, 57, 45, 32: after tracing the 55 Strong threshold repeatedly through the prior month, the reading has now broken below the 40% boundary into Weak-environment territory for the first time in the sequence.

The mechanism is a broad loss of breadth and persistence. Last week’s reading already reflected a thinning of directional alignment; this week that thinning became a breakdown. Energy split internally as the petroleum complex fell hard while Natural Gas rallied in the opposite direction, Grains reversed down after a six-week run and fractured into oilseeds-up against grains-down, Soft commodities split between a Cocoa bounce and an Orange Juice collapse, and Meats extended lower but on diminished magnitude. The equity advance lifted breadth on the upside, yet the per-contract magnitudes outside Nikkei and Nasdaq were contained. The barometer measures the share of markets generating medium-to-strong trends regardless of direction, and with sector after sector resolving into two-way internal splits rather than uniform moves, that share has dropped sharply. The Falling Rapidly rate of change is the relevant tilt: it points to further downside in the reading rather than stabilisation, and frames the current environment as a poor one for trend capture in either direction.

SG Trend Index: +0.38% month to date and +10.55% year to date as of 29 May, compared with +1.19% MTD and +11.44% YTD at last week’s close. The fourth week of May trimmed a further 80 basis points off the MTD figure and roughly 90 off the YTD, a second consecutive weekly giveback. The erosion concentrated in two places: the Grains reversal, which turned a six-week long-side run into a sharp drawdown for systems carrying that exposure, and the continued two-way churn in Energy, where the petroleum decline rewarded short exposure but the Natural Gas spike cut the other way. Long-Equity persistence provided the main offset, while the rebound in bonds worked against systems still positioned short duration after the prior month’s sell-off. The YTD reading holds above the double-digit threshold but has now given back the bulk of May’s earlier gain, which frames the month as a round-trip rather than an extension of the year-to-date arc.

Weekly Asset Class Snapshot

Sector averages are simple equal-weighted means of the constituent contracts in each sector.

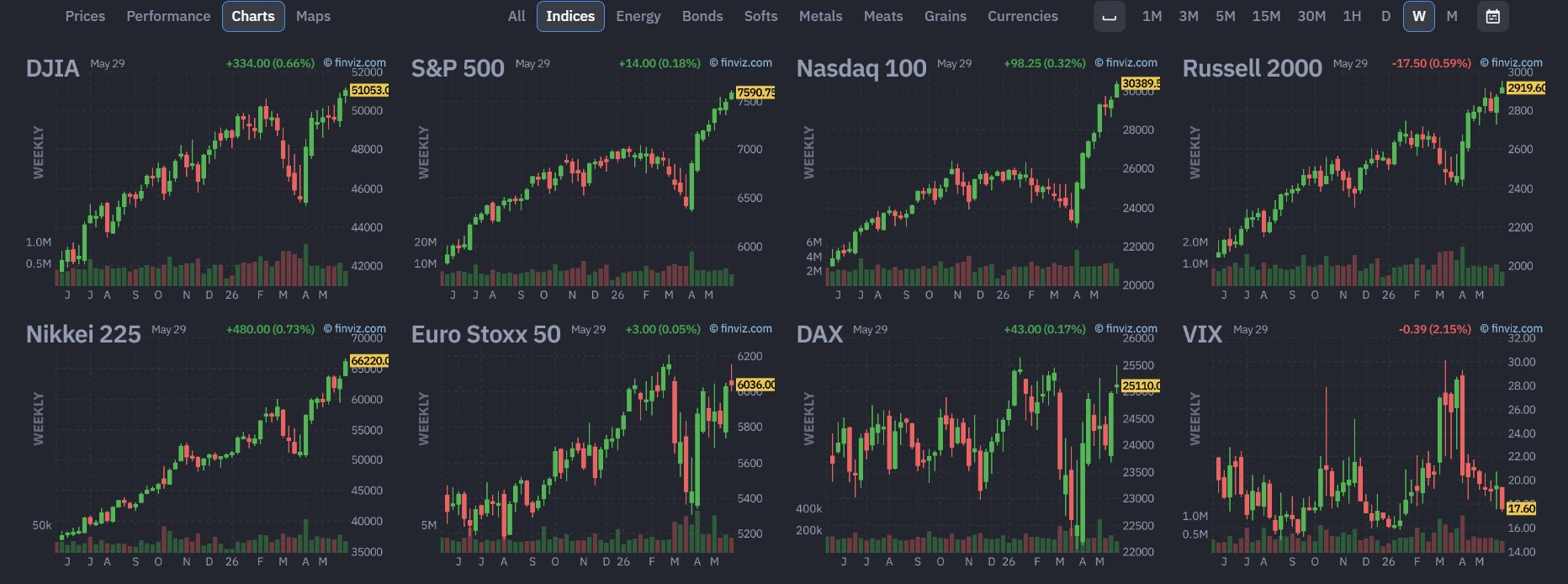

Equity Index (+1.84% | prev +2.40%)

All seven contracts higher again, extending the advance for a second week. Nikkei 225 led at +4.57%, Nasdaq 100 +2.86%, Russell 2000 +1.82%, S&P 500 +1.40%, DAX +0.84%, DJIA +0.82%, Euro Stoxx 50 +0.58%. The S&P closed green for a ninth consecutive week at a fresh record near 7591, and the Nasdaq 100 reached a new high near 30390, with reports attributing the leadership to continued strength in the AI-linked megacaps. Leadership rotated back toward Japan and US technology after the prior week’s European catch-up, the Nikkei near 66220 extending its multi-month uptrend. The advance was broad in direction but more contained in magnitude than the prior week, breadth holding intact while the per-contract moves narrowed.

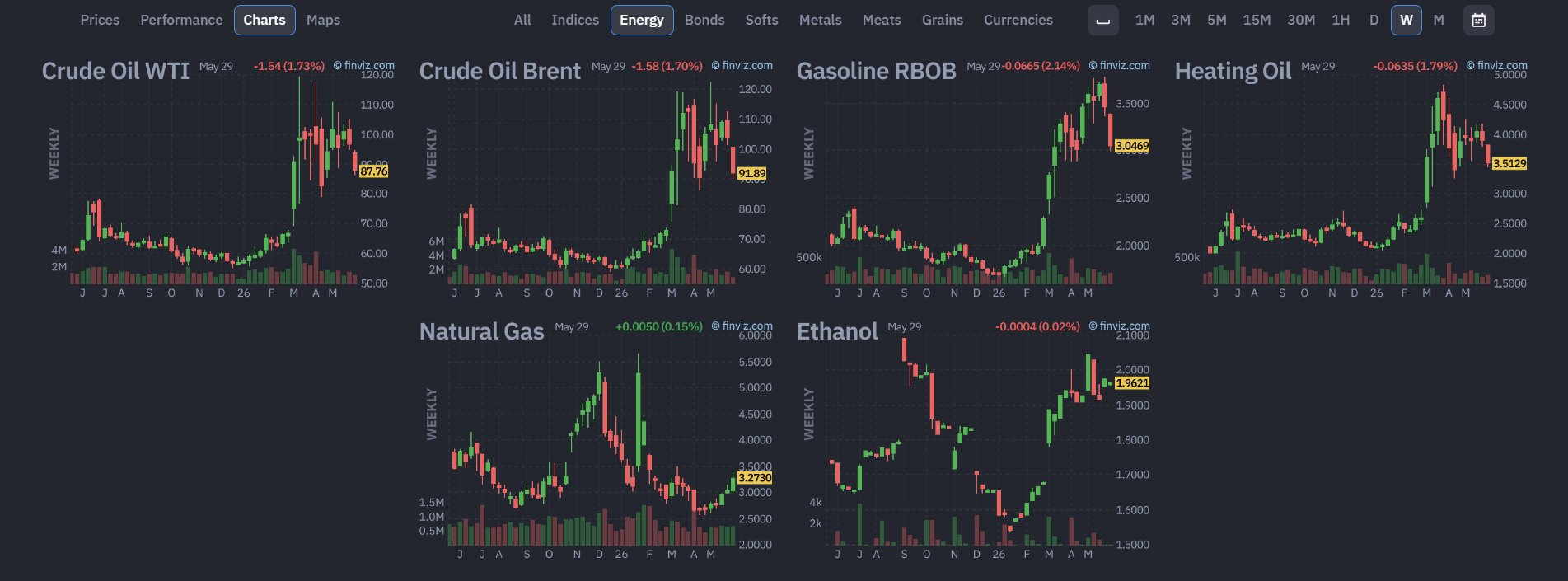

Energy (-5.12% | prev -3.30%)

A second consecutive decline, and the most internally split sector of the week. Four contracts fell hard: Crude Oil Brent -11.13%, Gasoline RBOB -10.23%, Crude Oil WTI -9.57% and Heating Oil -8.06%, with Ethanol -0.64% the fifth lower print. Natural Gas broke the opposite way at +8.90% to near 3.27, the single largest gain of the week, on reports of a bullish shift in summer cooling-demand forecasts and short covering unconnected to the petroleum story. The petroleum decline reflected a further unwind of the war-supply premium that had carried Brent toward 138 in April: market pricing reflected returning Middle East production and Strait of Hormuz traffic normalising, even as intermittent strike headlines kept intraday swings sharp. WTI near 88 and Brent near 92 have now retraced the bulk of the spring spike. For a sector that earlier in the year produced clean multi-week directional moves, the resolution into a petroleum-down, gas-up split is the relevant context: the directional opportunity sits on both sides, but no longer in a single sector-wide trend.

Metals (-0.02% | prev -1.70%)

A pull back to roughly flat after two weeks lower. Gold firmed +0.81% to near 4570 and Copper added +0.16% near 6.39, while Palladium -0.11%, Silver -0.43% and Platinum -0.53% eased on reduced magnitude. The sector average of -0.02% understates a now-mixed internal picture: the precious complex has stopped extending lower as the dollar softened and yields eased, and Gold has firmed off the prior weeks’ giveback while still sitting well below its January 2026 high. Copper near the upper end of its multi-month range maintains the industrial-side firmness. The two-week decline has effectively halted rather than reversed, leaving the complex without a single clean directional read at the sector level.

Soft Commodities (-1.98% | prev -0.68%)

The internal split inverted from last week. Cocoa rebounded +3.35% to near 3901 and Lumber added +0.34%, while Orange Juice reversed hard at -7.12% to near 159, Sugar -4.35%, Coffee -2.48% and Cotton -1.64%. The Orange Juice move gave back the prior week’s counter-trend bounce in full and re-established the broader downward path that has held since the 2024 weather-driven highs. Cocoa near 3901 has bounced off the prior multi-month base, the second sharp two-way swing in the contract in as many weeks. The sector read stays mixed at the contract level, with the directional opportunities running in opposite directions inside the same sector.

Grains (-1.12% | prev +1.24%)

The six-week positive run reversed. The sector fell -1.12% with six of eight contracts lower and a wide oilseeds-versus-grains split. Soybean Oil led the upside at +5.06% near 77.66 and Canola added +1.43% near 760.80, while Wheat fell 5.53% near 610, Corn 3.56% near 447, Rough Rice 2.93%, Oats 1.98%, Soybeans 0.81% and Soybean Meal 0.63%. Wheat was the weakest contract, giving back the bulk of its recent recovery, and Corn reversed sharply from the prior week’s gain. The internal alignment has flipped from the prior week’s broad-based upside to a two-way split, with the oilseed-oil complex extending higher while the grains and protein pockets turned down. A reversal after six positive weeks is the type of break that tends to register hardest in trend-follower performance.

Meats (-0.51% | prev -3.17%)

A second consecutive decline, all three contracts lower again but on much reduced magnitude. Lean Hogs fell 0.90% near 99.78, Feeder Cattle 0.41% near 348.93 and Live Cattle 0.23% near 239.20. The sector average of -0.51% compares with -3.17% the prior week, so the synchronised down move has continued but slowed sharply. Live Cattle has steadied inside its recent range after the prior week’s sharper drop, and the cattle complex now sits closer to consolidating than to extending its decline. A move back higher from here would frame the prior week as the low of a two-week pullback rather than the start of a sustained reversal in the multi-month structure.

Bonds (+0.71% | prev +0.13%)

Firmed across the curve for a second week, with the long end leading. The 30 Year Bond rose +1.35%, the 10 Year Note +0.76%, the 5 Year Note +0.51% and the 2 Year Note +0.21%. The bid reflected a softer-data, softer-inflation tilt: April PCE printed slightly below expectations on the month and the second-estimate Q1 GDP was revised lighter, allowing 10 year yields to ease further. The 30 year near 112.50, the 10 year near 109.88, the 5 year near 107.24, the 2 year near 103.30. After the prior month’s sell-off, the complex has put together two firmer weeks, turning the earlier break to lower prices into a recovery rather than a sustained duration setback. The curve steepened modestly as the long end outpaced the front, a move consistent with the easing inflation impulse from the falling petroleum complex.

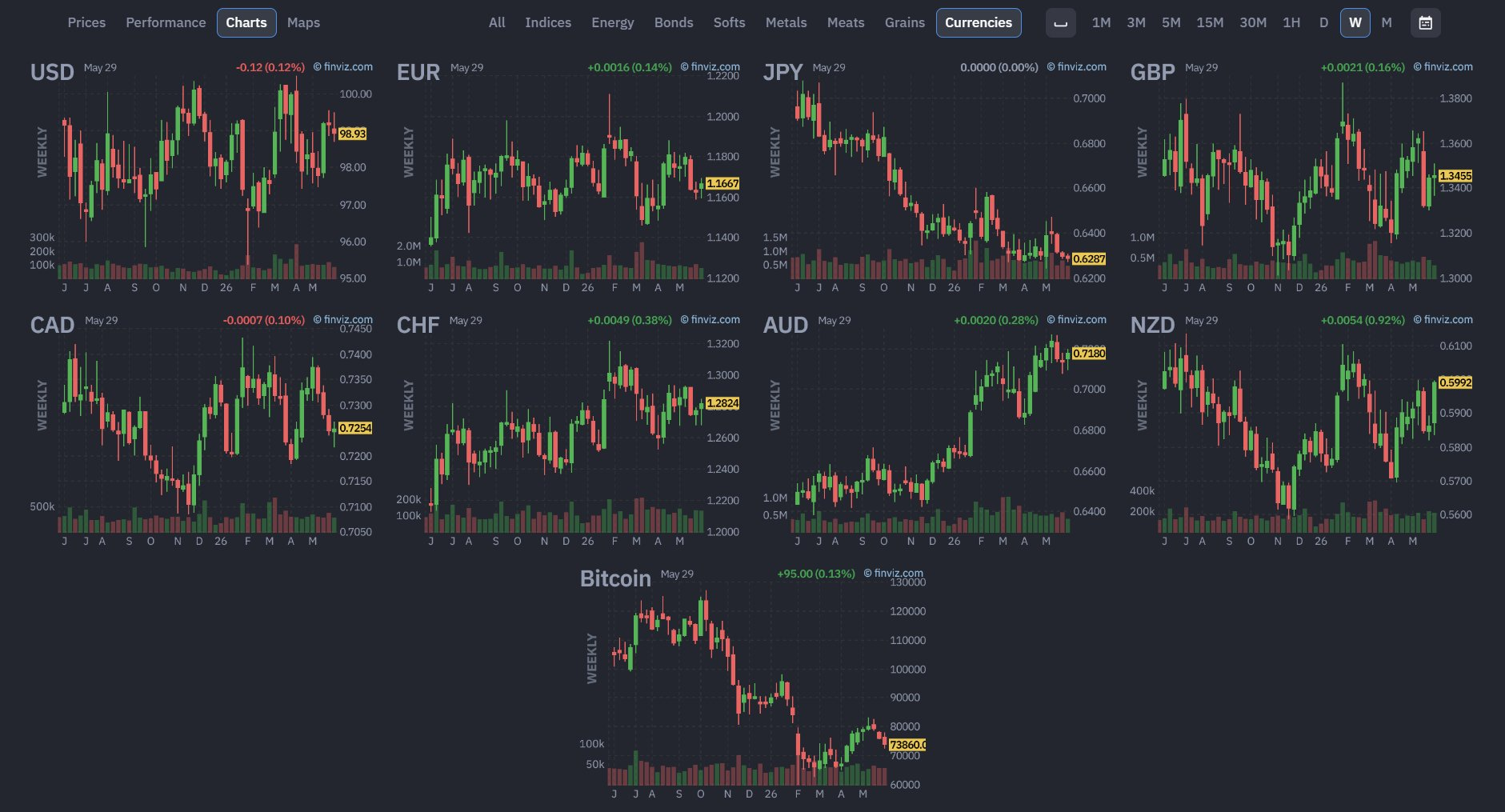

Currencies (+0.41% | prev +0.05%)

The dollar extended lower at -0.34%, a second consecutive softer-dollar week. The commodity-linked currencies led despite the oil decline, NZD +2.13% and AUD +0.63% the firmest, with EUR +0.42%, CHF +0.37%, GBP +0.10% and CAD +0.08% also higher; only JPY -0.14% sat marginally lower against the dollar. The USD index near 98.93 has now broken below the range that held through the strong-dollar phase, with the softer US data and easing yields removing the prior support. The read at the basket level has tilted toward a weak-dollar regime for the first time in several weeks, with the commodity currencies leading rather than the European pair, a rotation that sits alongside the firmer risk tape and the easing front end.

Volatility, Crypto: VIX fell a further 9.95% to near 17.60, a second large weekly decline that has pulled implied equity volatility back toward the lower part of its normal regime as the equity advance continued and the petroleum-driven risk premium drained out. Bitcoin fell 3.06% to near 73,860, extending its drift lower and now down roughly 38% from the January 2026 high near 120,000. The contract has continued to track risk-asset behaviour selectively and has not joined the equity advance, leaving its downward path intact.

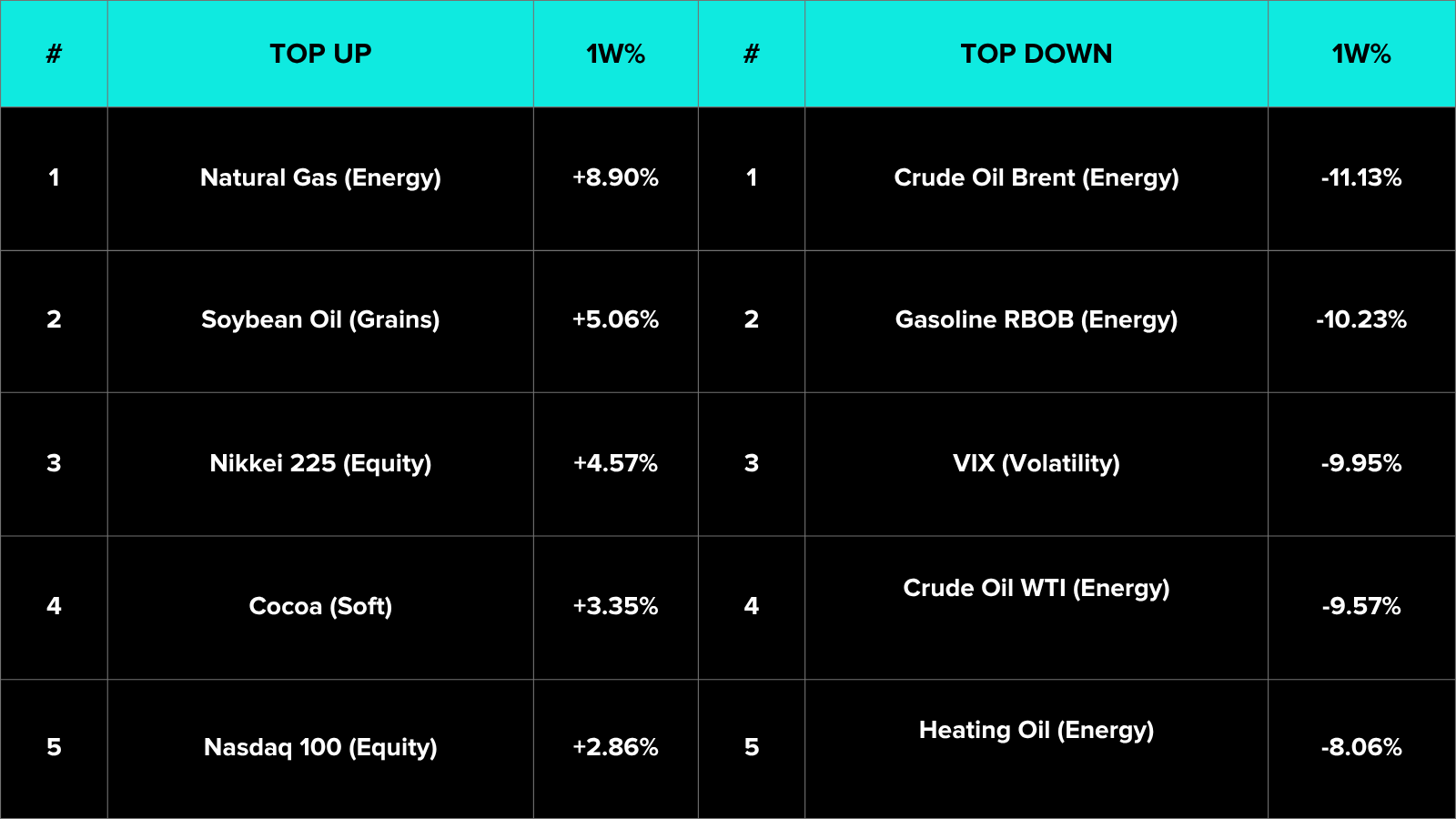

Top Movers

Top five up and top five down by single-week percentage move.

The composition tells a two-sided story. The downside list is dominated by the petroleum complex, four of the five largest declines (Brent, Gasoline RBOB, WTI and Heating Oil), framed by the VIX collapse. The upside list is broader and crosses sectors: Natural Gas leads as the single largest gainer, sitting in the same Energy sector as the four largest losers, followed by Soybean Oil, two equity indices and Cocoa. The signal sits in the divergence within sectors rather than across them: Energy split hardest, Grains and Soft commodities each resolved into opposing contract-level moves, and the only uniform-direction sector left on the board was equities to the upside.

Portfolio View

Portfolios positioned short the petroleum complex captured a second week of directional contribution, while any long Natural Gas exposure cut the other way inside the same sector. Long-Equity exposure extended its contribution for a second week as the indices advanced with breadth, and short-USD positioning added as the dollar broke lower. The detractors clustered in the trend breaks: long-Grains exposure, carried through a six-week run, absorbed a sharp reversal, and systems positioned short duration after the prior month gave back ground as bonds firmed. The pattern rewards bidirectional capacity in Energy and cross-sector diversification over single-direction concentration; the contracts that hurt most were those where a multi-week trend reversed inside the week rather than those that simply paused.

Final Reflections

The week ending 29 May 2026 extended the prior week’s direction rather than reversing it, but the internal structure deteriorated. The petroleum complex pulled the war-supply premium further out of crude, Natural Gas broke the opposite way, the inflation impulse softened, the long end of the curve firmed, the dollar broke lower, and equities advanced to fresh records. The TTU Barometer dropped from 45% to 32%, out of Neutral and into Moderately Weak, the SG Trend Index gave back a second consecutive 80 to 90 basis points to sit at +10.55% YTD, and contract-level breadth was close to even at 24 of 49 positive against 25 negative. The result is a market that is moving, in places sharply, but resolving into two-way internal splits sector by sector rather than the uniform directional trends that trend-following depends on.

1. The barometer’s break below 40% is the first genuine Weak-environment reading of the sequence, and the Falling Rapidly tilt points lower still.

The five-week sequence (55, 43, 57, 45, 32) has stepped down decisively after a month of repeatedly testing the 55 Strong threshold from below. The move out of Neutral into Moderately Weak, combined with a rate of change that accelerated from Falling Moderately to Falling Rapidly, tilts the evidence toward a further step down rather than a bounce. The relevant read for next week is whether 32 marks a near-term low in the indicator or the start of an extended cold phase: either resolution carries weight after a fortnight in which sector after sector has fractured internally. The structural signal is the more important one: when the share of markets in clean medium-to-strong trends falls this far, the environment penalises trend entries in both directions until persistence returns.

2. The petroleum complex has now logged two consecutive multi-week-scale declines, converting a former clean trend into a two-way headline-driven unwind.

Brent has retraced from an April peak near 138 back toward 92, and the past fortnight has produced declines of roughly 5% and 11% in succession as market pricing reflected the steady normalisation of Middle East supply, punctuated by intermittent strike headlines that kept intraday volatility high. For a sector that drove clean directional trends through the spring, the conversion to headline-driven two-way movement is the relevant context, and the simultaneous Natural Gas spike on a weather-forecast shift underscores that the sector is no longer trending as one. Trend-following systems can capture neither the petroleum reversal nor the gas spike cleanly; the configuration rewards reduced single-sector concentration and bidirectional capacity. The steadier cross-asset opportunity sits where the moves have been more consistent: the equity advance, the softer dollar, and the firmer front-to-long curve.

For trend followers, the week was not defined by whether markets rose or fell. It was defined by whether the moves were persistent enough to be captured. The opportunity was directional, but not directionally biased.

One question defines the week ahead: does the petroleum unwind and the equity advance settle into a steadier multi-week regime as the supply shock fades, or does the barometer’s drop into Moderately Weak prove the leading signal, with the internal splits spreading into the cross-asset moves that have so far held their direction?

List of Resources used in the Week in Review

Important Disclaimers

This document is directly solely to Accredited Investors, Qualified Eligible Participants, Qualified Clients and Qualified Purchasers. No investment decision should be made until prospective investors have read the detailed information in the fund offering documents of any manager mentioned in this document. This document is furnished on a confidential basis only for the use of the recipient and only for discussion purposes and is subject to amendment This document is neither advice nor a recommendation to enter into any transaction. This document is not an offer to buy or sell, nor a solicitation of an offer to buy or sell, any security or other financial instrument. This presentation is based on information obtained from sources that TopTradersUnplugged (“TTU”) (“considers to be reliable however, TTU makes no representation as to, and accepts no responsibility or liability for, the accuracy or completeness of the information. TTU has not independently verified third party manager or benchmark information, does not represent it as accurate, true or complete, makes no warranty, express or implied regarding it and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use.

All projections, valuations, and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein. Such projections, valuations and analyses may be based on subjective assessments and assumptions and may use one among many alternative methodologies that produce different results accordingly, such projections, valuations and statistical analyses should not be viewed as facts and should not be relied upon as an accurate prediction of future events. There is no guarantee that any targeted performance will be achieved Commodity trading involves substantial risk of loss and may not be suitable for everyone

TTU is not and does not purport to be an advisor as to legal, taxation, accounting, financial or regulatory matters in any jurisdiction. The recipient should independently evaluate and judge the matters referred to herein. TTU does not provide advice or recommendations regarding an investor’s decision to allocate to funds or accounts managed by any manager (“or to maintain or sell investments in funds or accounts managed by any manager, and no fiduciary relationship under ERISA is created by the investor investing in funds or accounts managed by any manager, or through any communication between TTU and the investor

In reviewing this document, it should be understood that the past performance results of any asset class, or any investment or trading program set forth herein, are not necessarily indicative of any future results that may be achieved in connection with any transaction. Any persons subscribing for an investment must be able to bear the risks involved and must meet the suitability requirements relating to such investment. Some or all alternative investment programs discussed herein may not be suitable for certain investors This document is directed only to persons having professional experience in matters relating to investments. Any investment or investment activity to which this document relates is available only to such investment professionals. Persons who do not have professional experience in matters relating to investments should not rely upon this document.

This document and its contents are proprietary information of TTU and may not be reproduced or otherwise disseminated in whole or in part without TTU’s prior written consent.

This document contains simulated or hypothetical performance results that have certain inherent limitations AND SHOULD BE VIEWED FOR ILLUSTRATIVE PURPOSES. Unlike the results shown in an actual performance record, these results do not represent actual trading. HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR INVESTMENT ACCOUNT.

ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT IN ADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING FOR EXAMPLE, THE ABILITY TO WITHSTAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM OR OTHER ASSET.

There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading results. No representation is being made that any investment will or is likely to achieve profits or losses similar to those being shown.

Most Comprehensive Guide to the Best Investment Books of All Time

Most Comprehensive Guide to the Best Investment Books of All Time

Get the most comprehensive guide to over 600 of the BEST investment books, with insights, and learn from some of the wisest and most accomplished investors in the world. A collection of MUST READ books carefully selected for you. Get it now absolutely FREE!

Get Your FREE Guide HERE!